Financing Land & Home Construction: What Buyers Should Know

At a Glance: Financing land and building a home on it are two separate processes, and understanding how they work together saves you time, money, and headaches. Whether you’re buying a rural acreage, a recreational property, or a plot of land to build your dream custom home, here’s what Nebraska buyers should know before they start.

Buying land and building on it isn’t the same as buying an existing home with a traditional mortgage. The financing works differently, the timeline is longer, and the details matter, especially in a rural area like much of Nebraska. From land loans and construction loans to permits and lender expectations, this guide walks through the process step by step so you can plan smart and build with confidence.

Why Financing Land Is Different From Financing a Home

Lenders See Land Differently

Most buyers are familiar with a typical mortgage: you find a home, get approved, close, and start making a monthly payment. Financing a land purchase doesn’t work the same way. Lenders see vacant land, especially raw land or undeveloped land without a structure, as a riskier asset. There’s no existing collateral the way a finished home provides, so:

- Interest rates tend to be higher

- Down payment requirements are steeper

- Loan terms shift depending on the type of land and what you plan to do with it

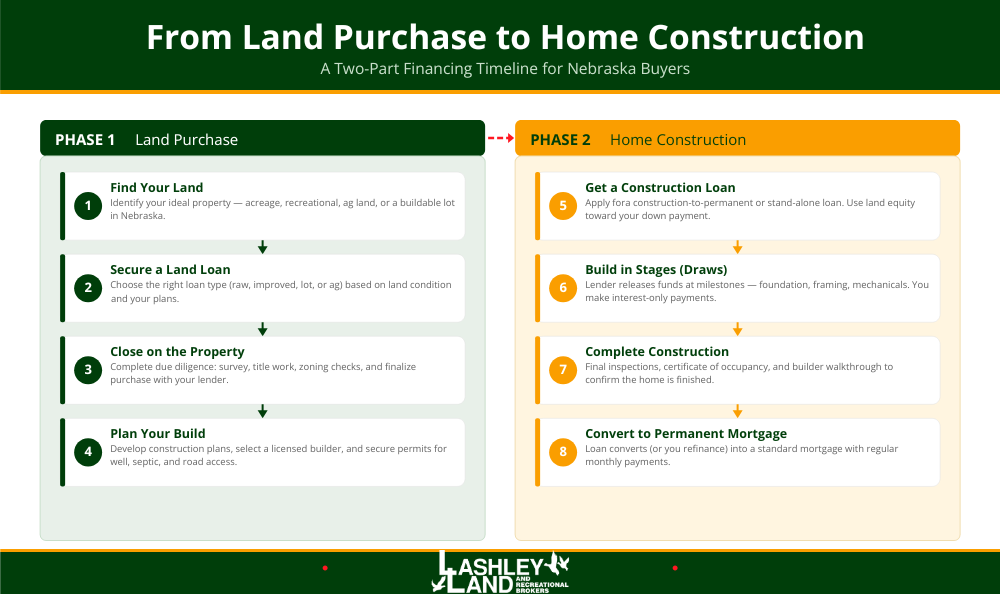

The Two-Part Reality

Buying the land is step one. Home construction is step two. Each phase often requires its own financing — or a loan product designed to combine both. Understanding this two-part process upfront helps buyers plan realistically and avoid surprises down the road.

Types of Land Loans Nebraska Buyers Should Know

Not all land loans are created equal. The type of loan you qualify for depends largely on the condition and intended use of the property.

Raw Land Loans

- For unimproved land with no utilities, roads, or structures in place

- Carries the highest down payments and the highest interest rate among land loan options

- Common for buyers purchasing recreational land, hunting ground, or long-term investment properties

- Lenders typically want to see a clear plan for the property before approving financing

Improved Land Loans

- Cover properties with some infrastructure — road access, utilities nearby, or basic improvements that make the land buildable

- Terms tend to be better than raw land loans

- More lender options available, especially through ag lenders and local banks that understand rural property

Lot Loans

- Apply to platted lots in subdivisions or developed areas

- Usually come with shorter terms, often two to ten years, with the expectation that you’ll build

- Local banks and credit unions familiar with the area are often the best source for a lot loan

Agricultural Land Loans

- Built specifically for productive farm and ranch ground

- Farm Credit Services, FSA programs, and local ag banks specialize in evaluating agricultural income, soil quality, and water rights

- These lenders understand the nuances of ag property in ways national banks simply don’t

- Lashley Land’s relationships with ag lenders across Nebraska can help connect buyers with the right financing options for their situation

Financing the Build: Construction Loans Explained

How Construction Loans Work

A home construction loan is a short-term loan that covers the cost of building your new home. Unlike a traditional mortgage, funds aren’t disbursed all at once. Instead, the lender releases money in stages — called draws — as construction milestones are completed. During the construction phase, you’ll typically make interest-only payments rather than full principal-and-interest payments.

Construction-to-Permanent Loans

- Combines the construction loan and the permanent mortgage into one product

- One closing, one set of fees — simpler for the buyer

- Not all lenders offer a construction-to-permanent loan for rural properties, so working with the right lender matters

Stand-Alone Construction Loans

- A separate loan just for the build phase

- Once the home is finished, you refinance into a permanent mortgage

- Two closings and two sets of costs, but it can offer more flexibility during construction

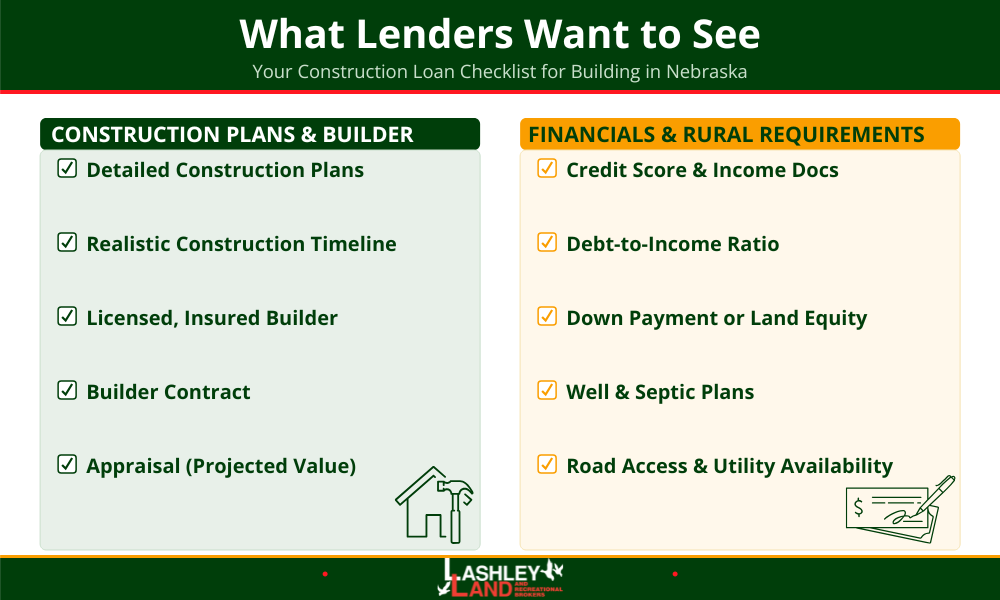

What Lenders Want to See

Regardless of which route you take, expect lenders to review:

- Detailed construction plans and a realistic timeline

- A licensed, insured builder with a solid track record

- An appraisal based on the projected completed value of the new home

- Your financial qualifications — credit score, income, and debt-to-income ratio

- For rural builds: well and septic plans, road access, and utility availability

Combining Land and Construction Financing

Buying Land and Building in One Transaction

Some lenders offer land-and-construction combo loans that cover both the land purchase and the construction cost in one package. These are ideal for buyers who find the right property and are ready to build right away. They typically require a builder contract and construction timeline at the time of your loan application.

Buying Land Now, Building Later

Many Nebraska buyers purchase land first and build down the road. In that case, you’ll finance the land separately and apply for a construction loan when you’re ready to break ground. A few things to keep in mind:

- Pay close attention to your land loan terms — balloon payments and shorter repayment windows can affect your timeline for permanent financing

- Even if construction is a few years out, having a general plan strengthens your position with lenders

Using Land Equity as a Down Payment

- If you own your land free and clear or have significant equity, many lenders will count that toward the down payment on your construction loan

- This can reduce or eliminate the cash you need upfront for the build

- It’s an especially common strategy in rural Nebraska for families building on inherited or long-held land

Nebraska-Specific Considerations

Working With Ag Lenders and Local Banks

Farm Credit institutions, local community banks, and ag-focused lenders understand how to evaluate land with irrigation, water rights, CRP contracts, and agricultural income. They speak the language of rural real estate in ways large national lenders typically don’t. Lashley Land’s long-standing relationships with these lenders help buyers navigate the process from start to finish.

Rural Building Realities

Building in rural Nebraska comes with additional expenses and logistics that buyers should plan for:

- Well and septic systems, rural electric connections, and road access all add to the timeline and cost

- County zoning and building permit requirements vary — getting the necessary permits in place early prevents delays

- Flood plains, soil conditions, and water table depth can impact where and how you build, which is why a thorough land survey is an important early step

Programs and Resources Worth Knowing

- USDA Rural Development loans — designed for rural homebuyers, often with low or no down payment requirements

- FSA programs — support for beginning farmers and ranchers

- Nebraska-specific grants or incentive programs for rural housing may be available depending on your location and situation

- A knowledgeable broker or lender can help identify which programs you qualify for — and that guidance alone can make a meaningful difference in your financing

Working With the Right Team

Why Your Broker Matters

A land-specialized real estate agent or broker understands the financing landscape for rural and agricultural property in ways a general residential agent may not. They can identify potential issues — easements, water rights, zoning restrictions — before they become deal-breakers. Lashley Land’s team works alongside buyers from property search through closing, including connecting them with the right lenders and professionals.

Other Professionals You’ll Need

- Ag lender or loan officer experienced with land and construction loans

- Builder licensed and experienced in rural construction

- Attorney for contract review, title work, and easement questions

- Surveyor to confirm boundaries and identify buildable areas

- Tax advisor who understands property tax implications and any agricultural exemptions

Having the right people in your corner from the beginning keeps the construction process on track and helps you avoid costly missteps.

Plan Smart, Build With Confidence

Financing land and home construction takes more careful planning than a standard home purchase, but it’s very doable with the right information and the right team guiding you. Nebraska offers strong opportunities for buyers looking to build in a rural area, whether it’s a primary residence, a weekend retreat, or a working farm.

Lashley Land brings over 140 years of combined experience in Nebraska land sales. Whether you’re looking for the right property or need help navigating the financing process, we’re here to help. Contact Lashley Land today to talk through your goals.