1031 Exchange Into a 721 Exchange: How to Defer Capital Gains on a Land Sale

This article is for informational purposes only and does not constitute tax advice or legal advice. Consult a qualified tax professional and attorney before executing any exchange strategy.

Nebraska landowners with appreciated farmland, ranches, or recreational property often face the same dilemma: sell and lose a significant chunk to capital gains taxes, or hold on longer than they’d like.

There is a middle path. A 1031 exchange defers capital gains taxes by rolling your sale proceeds into a like-kind replacement property. A 721 exchange, also called a UPREIT transaction, then allows you to contribute that replacement property to a real estate investment trust’s operating partnership in exchange for partnership units. The result: an illiquid land asset converts into diversified, passive income without triggering a taxable event at either step.

Used in sequence, these two strategies create a powerful tax deferral and estate planning path for Nebraska land sellers. Here is how each one works, how they connect, and how to know if the combination makes sense for your situation.

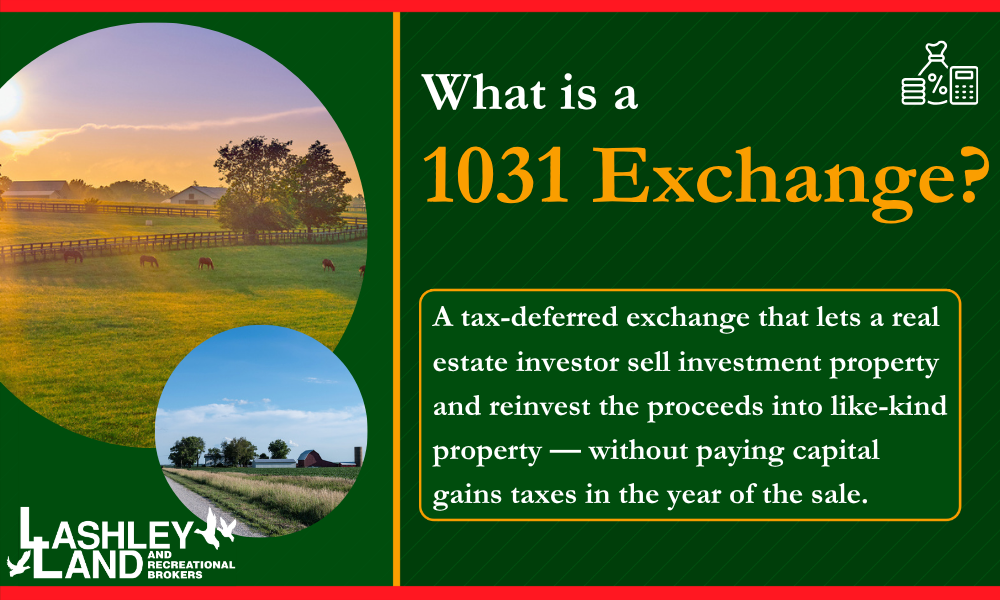

What Is a 1031 Exchange and Why Land Sellers Use It

A 1031 exchange is a tax-deferred exchange authorized under Internal Revenue Code Section 1031. It allows a real estate investor to sell investment property and reinvest the sale proceeds into like-kind property without paying capital gains taxes in the year of the sale. The capital gain is deferred, not eliminated, but that deferral can be worth a great deal when Nebraska farmland values have appreciated significantly over decades of ownership.

The exchange process follows a specific set of steps with strict deadlines:

- Sell the relinquished property — the land, farm, or ranch you are exiting

- A qualified intermediary, sometimes called an exchange facilitator, holds the exchange funds in a segregated escrow account; you cannot take personal receipt of the proceeds

- Within the 45-day identification period after closing, you must identify potential replacement properties in writing

- You must close on the new property within 180 calendar days of the original sale

To qualify under IRS rules, both the relinquished property and the replacement property must be real property held for productive use in a trade or business or for investment. The replacement property must be of equal or greater value to defer the full capital gain. Primary residences and personal property do not qualify.

Common disqualifiers include missing the strict deadlines, taking personal receipt of exchange funds before the exchange is complete, and using the replacement property as a primary residence or personal property. Working with an experienced qualified intermediary from the start protects against most of these pitfalls.

What Is a 721 Exchange (UPREIT Transaction)?

A 721 exchange is authorized under IRC Section 721 and works differently from a 1031. Rather than selling one real property and buying another, a real estate owner contributes real property directly to a real estate investment trust’s operating partnership in exchange for operating partnership units, often called OP units.

It is not technically a like-kind exchange. It is a contribution to a business entity. But like a 1031, it is a tax-deferred transaction under the right conditions. The capital gain on the contributed property is not recognized at the time of contribution.

The benefits of a 721 exchange appeal to landowners who are ready to step away from active management:

- Tax deferral. The capital gain built up in the contributed property is deferred as long as you hold the OP units.

- Passive income. OP units generate distributions from the REIT’s portfolio, which typically spans commercial real estate, multifamily apartment buildings, industrial properties, and other asset classes across the United States.

- Diversification. Instead of holding a single piece of real property, you hold beneficial interests in a broadly diversified real estate portfolio.

- Estate planning advantages. When OP units pass to heirs, those heirs may receive a stepped-up basis, potentially eliminating the deferred capital gain entirely at death.

There are meaningful limitations to understand as well. OP units are not liquid the way publicly traded stock is. Holding period restrictions apply. Once you contribute the property, you give up direct ownership and control over that specific asset. REIT performance depends on market conditions, and past performance does not guarantee future results. These are specific requirements and specific rules that a qualified tax advisor should walk you through before you commit.

How a 1031 Exchange and a 721 Exchange Work Together

The important thing to understand is that these are sequential strategies. The 721 exchange is an exit strategy from the replacement property you acquired in the 1031. It is not an immediate follow-on to your original land sale.

Here is why that matters for Nebraska agricultural landowners: you generally cannot contribute farmland or ranch land directly to a REIT’s operating partnership and claim tax deferral. Contributing exchange property that has not been held as an investment for a sufficient period is typically treated as a taxable event. The 1031 exchange is the bridge that gets you from raw agricultural land into a property type that can later be contributed via a 721 exchange.

The full sequence looks like this:

- Sell the relinquished property, whether that is cropland, a cattle ranch, or recreational ground

- A qualified intermediary holds your exchange funds, keeping you out of receipt and preserving the deferred exchange status

- Within the 45-day identification period, identify like-kind property as your replacement property

- Close on the replacement property within 180 calendar days

- Hold the replacement property for a sufficient period to establish investment intent; most tax advisors recommend a minimum of one to two years, though there is no bright-line IRS rule or formal safe harbor that specifies an exact holding period

- Contribute the replacement property to a REIT’s operating partnership through the 721 exchange in exchange for OP units

- Begin receiving passive income distributions while the capital gain remains deferred

There is no exchange accommodation titleholder involved in the 721 step the way there might be in a reverse exchange. The 721 contribution is a straightforward transfer of real property to the operating partnership for OP units.

The tax year in which you execute each step matters for reporting purposes, and a qualified intermediary and tax advisor should be coordinating with you throughout.

Is This Strategy Right for Nebraska Land Sellers?

This combination of strategies is not for everyone, but it is well-suited to a specific type of Nebraska real estate owner.

It tends to be a good fit if:

- You are a landowner exiting active farm or ranch management and want to replace rental income or cash rent payments with passive distributions

- You own highly appreciated property and are facing a large capital gain tax bill plus depreciation recapture tax on improvements or equipment

- You are an estate executor or heir looking for a clean, tax-efficient way to exit an inherited land position without triggering a large capital gains tax event

Think carefully if:

- You need near-term liquidity; OP units are not cash, and converting them takes time

- Your goals require maintaining control over a specific real estate asset or parcel

- You are considering this strategy for a primary residence or personal property, which does not qualify

Nebraska-specific considerations:

Agricultural land values across Nebraska have risen substantially over the past decade, making capital gains taxes on a sale a real consideration. The combination of federal rates and Nebraska state taxes makes deferral strategies worth serious attention.

A few things deserve careful review before any exchange:

- Water rights and mineral rights associated with the property can affect whether the exchange qualifies and how it gets structured

- Holding periods, sequencing, and transaction details all carry real consequences — working with a qualified intermediary and tax advisor experienced in Nebraska agricultural real estate is not optional

The team at Lashley Land has worked with Nebraska landowners across farmland, ranch, and recreational property sales. For farmers who want to unlock equity without walking away from the land, Lashley Land’s Fractional Farm Ownership Program offers a leaseback option worth exploring alongside these strategies.

Key Terms Every Land Seller Should Know

1031 Exchange — A tax-deferred exchange under Internal Revenue Code Section 1031 that allows a real estate investor to sell investment property and roll sale proceeds into like-kind property without recognizing the capital gain in that tax year.

721 Exchange / UPREIT Transaction — A contribution of real property to a REIT’s operating partnership in exchange for OP units, authorized under IRC Section 721 and structured as a tax-deferred transaction.

Qualified Intermediary — A neutral third party, also called an exchange facilitator, who holds exchange funds in an escrow account during a 1031 exchange. Required for a valid deferred exchange; the seller cannot take receipt of funds.

Relinquished Property — The real property being sold in a 1031 exchange, such as a Nebraska farm, ranch, or recreational parcel.

Replacement Property — The like-kind property acquired with the exchange funds; must be of equal or greater value to defer the full capital gain.

45-Day Identification Period — The window after closing on the relinquished property during which you must identify potential replacement properties in writing.

OP Units — Operating partnership units received in a 721 exchange, representing beneficial interests in the REIT’s operating partnership and entitling the holder to distributions.

Depreciation Recapture Tax — Tax owed on depreciation deductions taken during the ownership period. A 1031 exchange defers this tax, but does not eliminate it.

Holding Period — The time a property must be held to demonstrate investment intent. Relevant to both the replacement property in a 1031 and the exchange property contributed in a 721.

Like-Kind Exchange — The broader category of tax-deferred exchange under IRC Section 1031; the term refers to the nature of the transaction, not necessarily the property type, as most real property in the United States qualifies as like-kind to other real property.

Selling Nebraska Land Doesn’t Have to Mean a Big Tax Bill

A 1031 exchange defers capital gains taxes by rolling your sale proceeds into a replacement property. A 721 exchange later converts that like-kind property into OP units, delivering passive income, diversification, and continued tax deferral with meaningful estate planning upside.

These are sophisticated strategies. Sequencing matters. Holding periods matter. The specific rules governing each transaction matter. None of this is a substitute for qualified tax and legal advice tailored to your situation.

But for Nebraska landowners who are ready to exit a farm, ranch, or recreational property, understanding how a 1031 exchange and a 721 exchange work together is a good place to start.

Thinking about selling farmland, a ranch, or recreational property in Nebraska? Contact Lashley Land to talk through what your land is worth and what your next move could look like.